REQUIREMENTS

REGISTRATION

Registration at the Chamber of Commerce

AFTER REGISTRATION

After the company incorporation

BV - private limited company in the Netherlands

The BV is a private limited company in the Netherlands. It is also called a Ltd., limited company or Besloten vennootschap. It is the most common legal structure for foreign companies expanding to the Netherlands and a very popular legal form for new companies in the Netherlands.

Requirements to incorporation of a BV company:

Incorporating a BV is a fairly straight-forward process. Basically everyone can open their own Dutch private limited. Take the following requirements into account:

- The BV needs to hold a valid and unique business name.*

- 0,01 euro (so only 1 eurocent) minimum share capital.

- The Articles of Association and a Deed of Incorporation (in Dutch) must be drafted before a public notary.

- The notary needs to be sure you understand what you are signing. Therefore, if you do not master the Dutch language, a translation or translator is required.

- A registered address in the Netherlands. This can be a residential, office or other type of address. We do recommend you to make sure that the business' address reflects the nature and scale of the business.

*Choosing a Business/Trade name

The name you select for your company has to be unique in the sector and geographical region you are operating in. Furthermore, the name of your business (for example "Legalee BV") cannot already be registered in the Chamber of Commerce register. You can find the register at kvk.nl and search if your business name is still available. The Kamer van Koophandel charges €50 for the registration. This a one-off payment. If you incorporate a BV company, the notary will take care of the registration but the fee will be charged to your company after the incorporation.

If your trade name is essential to your business it is recommended to register it as a trade mark in the Benelux (Belgium, the Netherlands and Luxembourg). You can search the database of the Benelux Office for Intellectual Property to see if yours is already taken. If your main focus area lies within several other countries within the European Union (EU) you can consider registering your trade name as a EU Trade Mark. In case your company will actively conduct business outside The Netherlands, Belgium and Luxembourg, you can additionally register your name/mark at the World Intellectual Property Organization (WIPO).

Requirements to trading with a BV company

To incorporate the company at the notary, meeting the criteria mentioned above is sufficient. However, your new company will need to meet some requirements to effectively run it: to obtain a VAT-number and open a bank account. Those requirements are called the substance requirements. These regulations are not strict laws, but they are increasingly important. These requirements include, but are not limited to, the following:

- At least half of the directors of the company should be resident of the Netherlands.

- The bookkeeping of the company must take place in the Netherlands.

- The company must comply with all its tax obligations in the Netherlands and is not treated as a tax resident of another country.

- The business address of the company is in the Netherlands.

- The Dutch resident directors should have the professional knowledge and skills to properly perform their duties. These duties at least include the decision making process regarding the company's transactions and follow-up.

- The company will have adequate support to run its business.

- The (most important) board decisions of the company are made in the Netherlands.

- The main bank accounts of the company are maintained from the Netherlands.

- The bookkeeping of the company must take place in the Netherlands.

- The company runs a real risk with respect to its financing, licensing or leasing activities. The company has an equity at risk that corresponds to the functions performed.

Failure to meet these requirements can lead to the company being denied a VAT/BTW number and/or a bank account. Banks usually require that at least one director is a Dutch resident. For these reasons NordicHQ recommends its clients to employ a Dutch resident (nationality not important) as one of its directors. Registering a company without a local director is technically possible but you would not meet the Substance Requirements, which can have the aforementioned consequences.

Local Director & "Substance" Requirements

"I strongly advise against setting up a BV without at least one Dutch-resident director. While a notary and the Chamber of Commerce might let you register, the Belastingdienst (Tax Office) and Dutch banks will likely block your VAT and account applications if they don't see a real local connection."

— Thomas, Legal & Business Advisor

1. VAT Number Success

To be considered a 'tax resident,' at least half of your statutory directors should reside in NL. Without this:

- Your VAT (BTW) application may be rejected.

- You risk being seen as a 'shell company.'

- You may lose access to the 0% intra-community VAT rate.

2. Banking & KYC

Dutch banks are under strict AML (Anti-Money Laundering) pressure. They prioritize clients who:

- Have a local resident with signing authority.

- Can show physical operational activity in NL.

- Fulfill KYC checks via a local representative.

How to meet this requirement remotely:

If you aren't moving to the Netherlands yet, we recommend appointing a Local Director or a trusted local employee. We can assist in drafting an operational plan that shows the Belastingdienst exactly how your company will be managed from Dutch soil, even while you are abroad.

Different BV use cases

Holding BV:

This structure is used to hold shares in one or more subsidiaries, manage assets, or protect intellectual property rights. It can be beneficial for tax planning and risk management purposes. More below and in this guide.

Operating BV

This structure is used for conducting the primary business activities, such as providing goods or services. An operating BV focuses on day-to-day operations, including sales, marketing, and production.

Finance BV

This structure is employed to manage intra-group financing activities or act as a centralized treasury center for a group of companies. It can be advantageous for optimizing cash management and minimizing foreign exchange risks.

Intellectual Property (IP) BV

This structure is specifically set up to hold and manage intellectual property rights, such as patents, trademarks, or copyrights. The IP BV can help reduce tax exposure on royalty income and protect valuable assets.

Real Estate BV

This structure is used to hold and manage real estate assets, either for rental income or capital appreciation. A Real Estate BV can offer tax advantages and liability protection related to property ownership.

Medical BV

Specifically used by medical professionals, often working in or close with a hospital.

Structure

A Dutch private limited (BV) company can be structured in roughly two ways:

- A BV with a natural person or company as the shareholder.

- A BV holding structure consisting of a holding company that owns (part) of the shares in another bv, the operating BV.

Required Documents for BV Setup

"You don't need a mountain of paperwork. For a standard setup, we just need IDs and proof of address. The complexity only increases if you incorporate remotely or via a foreign holding company."

— Thomas, Legal & Business Advisor

The Standard Checklist (Everyone needs these):

- Passport Copy: For all directors and shareholders.

- Proof of Residence: Utility bill, bank statement, or phone bill (max 2 months old).

- Rental Agreement: For the registered office (unless using a shareholder's home address).

| Document Required | In Person (AMS) | Remote (POA) | Corporate Shareholder |

|---|---|---|---|

| Standard ID & Proof of Address | ✔ | ✔ | ✔ |

| Legalized/Apostilled Passport | ✕ | ✔ | ✔ |

| Power of Attorney (Legalized) | ✕ | ✔ | ✔ |

| UBO Declaration | ✕ | ✕ | ✔ |

| Legal Opinion (Apostilled) | ✕ | ✕ | ✔ |

Legalization & Apostilles

For Remote Incorporation

- Apostille: Required if your country signed the Apostille Convention. Validates the notary's signature.

- Consulate Legalization: Required if your country has not signed the convention.

- Online ID: In some cases, we can identify you via secure video call to skip the apostille.

Corporate Shareholder

(e.g., UK Ltd owning Dutch BV)

- Legal Opinion: Statement confirming your foreign entity exists and authorized signatories.

- UBO Declaration: Identifying the "Ultimate Beneficial Owner" (>25% shares).

- Datacard: Provided by our notary.

Dutch BV owned by foreign company

Many entrepreneurs own a BV in the Netherlands, but later on decide to transfer ownership of the BV to a foreign company. For example when headquarters is moved to another country but the Dutch operation needs to continue.

Another example is when the company is sold to a foreign entity. Also thinkable is that the main shareholder moves from the Netherlands to a new country. This can be the case when the shareholder moves personally to another country and it makes more sense to hold the shares in a new holding company in that new country of residence.

When you own the shares in a Dutch BV and you want to transfer ownership to a foreign entity, here is an example that might be helpful.

Transfer ownership of BV to a foreign entity

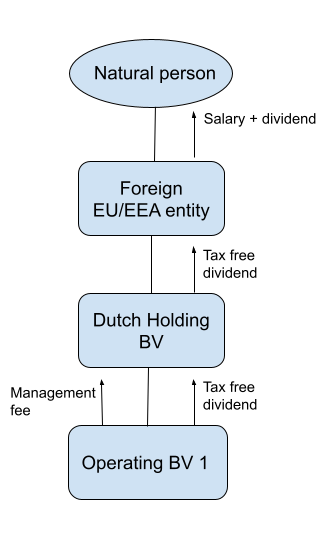

In our example the shares of a BV in the Netherlands are held 100 percent by a natural person, a Dutch resident with an EU/EEA-passport. He is also the managing director in this BV and has a fulltime employment contract with his own BV.

This person decides to move to Norway long term. For that reason it makes sense to receive a salary in Norway and use the social services there. In order to achieve that he needs to establish an AS (the Norwegian equivalent of a BV) in Norway and sell the shares of the Dutch BV to that entity.

Before we get into that we will need to determine both the tax consequences of emigration and opportunities to circumvent possible (future) Dutch tax levies. Below we will split the findings per tax type: personal income tax, corporate tax and dividend tax.

Personal income tax (Inkomstenbelasting, IB)

Once you have set up your company abroad and started employment for your own company there, you will stop paying personal income tax to the Netherlands. Instead, you will pay income tax and social security contributions in your new country.

The main fiscal rule for emigration is that the Tax Authorities can impose a so-called protective assessment (Dutch: conserverende aanslag). Meaning that the Dutch tax authorities can have a claim on some of your personal income. This applies also to those with a substantial interest (over 5%) shareholding in a company in the Netherlands. In practice it often does not mean that you will pay extra, but you need to pay attention to this rule at emigration from the Netherlands. If you are not personally migrating from the Netherlands but moving ownership of your Dutch company abroad, the protective assessment does not apply.

One extra thing you should look into is your health insurance. The moment you stop taxing to the Netherlands and start your employment abroad you normally also stop paying health insurance premiums in the Netherlands. Depending on the system of your specific country, you should arrange this yourself. In our Norwegian example, your health insurance is included in the social security premiums you pay on top of your personal income tax. Other than the Dutch system, health insurance is built into this and you do not pay additional premiums to a private insurer.

| Personal income tax | Taxable income | Tax rate |

|---|---|---|

| 22% municipal and national tax, plus: | 1. Income up to NOK 190,349 | 0 |

| 2. Income between NOK NOK 190,350 – 267,899 | 1.7% | |

| 3. Income between NOK 267,900 – 643,799 | 4% | |

| 4. Income between NOK 643,800 – 969,199 | 13.4% (residents of Finnmark and Nord-Troms 11.4%) | |

| 5. Income between NOK 969 200 – 1 999 999 | 16.4% | |

| Income over NOK 2,000,000 | 17.4% |

Corporate Tax (Vennootschapsbelasting, Vpb)

The Dutch BV is incorporated under Dutch law and is therefore subject to Dutch corporate income tax, regardless of where the actual management is located. So even if the main shareholder moves abroad and/or the BV will be owned by a foreign entity, the basic principle is that Dutch corporate tax is owed to the Dutch tax authorities.

Transferring profits from a daughter company to a mother company within the EU, normally means that you will only pay profit tax once (see also: participation exemption). In practice this usually means that you will pay profit tax on the profits in the Netherlands.

Norway is formally not a member of the EU and the EU Parent-Subsidiary Directive with regard to participation profits does not apply, but the relevant arrangement has been extended to Norway (and Iceland) by convention.

Paying corporate tax in the Netherlands is usually more beneficial than paying it in other countries.

| Profit | 2025 | 2026 |

|---|---|---|

| SME tariff | 19% (up to €200.000) | 19% (up to €200.000) |

| Standard tariff | 25,8% (profits exceeding €200.000) | 25,8% (profits exceeding €200.000) |

| Innovation Box | 9% on profits derived from qualifying innovative activities | 9% on profits derived from qualifying innovative activities |

Compare that to corporate tax in other countries:

| Country | Corporate Income Tax Rate | Patent Box Regime (R&D rate) | |

|---|---|---|---|

| Germany | 30% on average. Combination of federal and municipal tax. | - | 15% Federal + 5.5% Surcharge + ~14% Municipal (Trade Tax) |

| United Kingdom | 25% | 10% | 19% "Small Profits" rate applies to firms below £50,000 |

| France | 25-31% | 10% | Large Firms: Exceptional surtax for firms >€1B turnover (eff. rate ~28.4%–31%). |

| Italy | 28% approximately, based on national and regional taxes | - | Incentive Change: Replaced with a 110% Super-Deduction for R&D costs |

| Spain | 25% | 10% | 15% reduced rate for new companies (first 2 years of profit) |

| Portugal | 19% | 2.85% | Dropping from 20% in 2025. PB is an 85% exemption on the 19% rate |

| Ireland | 12.5% | 6.25% | 15% effective rate for firms >€750M revenue (Pillar Two) |

| Netherlands | 19 / 25,8% | 9% | 19% on first €200,000; 25.8% on the excess |

| Belgium | 25% | 3.75% | Effective via Innovation Income Deduction (85% of net IP income) |

| Sweden | 20.6% | - | No change |

| Norway | 22% | - | No change |

| Denmark | 22% | - | No change |

| Finland | 20% | - | Introduction of 250% superdeduction for university collabs. Announced corporate tax drop in 2027 |

| Estonia | 22% | - | Only CIT when profits distributed to shareholders |

| Latvia | 20% | - | Only CIT when profits distributed to shareholders |

| Lithuania | 17% | 6-7% | |

| Poland | 9% / 19% | 5% | 9% for small firms (<€2M turnover) |

Dividend tax (Dividendbelasting)

The goal is to transfer profits in the Netherlands to the new parent company. These kinds of profit distributions from the Dutch company to the shareholder (the foreign company) are called dividends. Dividends can be subject to taxation. Many countries have set up tax treaties to avoid major shareholders from having to pay these kinds of profit distributions which have already been taxed with corporate tax. The general rule within the EU is that a dividend paid from a BV to a shareholder that owns 10 percent or more is exempt from dividend tax.

To determine whether dividend tax is due we should always check any tax treaty. In our example we take a look at the Dutch-Norwegian tax treaty. Under the Netherlands-Norway tax treaty, distribution of dividend by a Dutch company to a company established in Norway is exempt from withholding dividend tax if the Norwegian company owns at least 10% of the share capital in the Dutch company.

In our example the Norwegian AS will own 100 percent of the shares. In other words: no dividend tax is due on dividends paid from the Dutch BV to the Norwegian AS.

Setting up the structure

Once you have established the tax implications of your emigration, you can start setting up the structure.

Start by setting up the foreign entity. This different per country. You can find a comprehensive guide for starting a company in Norway here. If you are setting up an entity in the Netherlands, find a step-by-step guide here. At the same time, visit the notary in the Netherlands to sell/transfer the shares from the Dutch BV to the foreign entity.

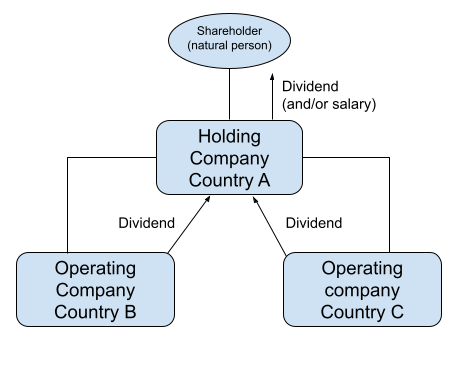

The standard structure most clients in the Netherlands work with is a so-called holding structure, consisting of a Holding BV and an Operating BV. The Operating BV is where the actual company activity takes place whereas the holding BV serves as the private investment/savings vehicle for the owner.

Taxation in the new structure

In the example where ownership of the Dutch structure is moved abroad, the new structure would look something like the below:

As explained, the goal is to "move profits up" the structure.

The Dutch Holding BV sends the Operating BV (where the "real" business activity takes place) management invoices. These management fees are seen as costs in the Operating BV and thereby decrease the amount taxable profit in the Operating BV. The management fees are taxable income in the Holding BV. Any profits in the Operating or Holding BV are subject to corporate tax in the Netherlands.

Alternatively you can send all profit generated in the Operating BV to the Holding BV in the form of dividends (profit distribution). Note: This is usually not possible if you have another shareholder in the Operating BV. In that case both shareholders in the Operating BV will send management invoices from their respective holding BV's. The Dutch tax authorities expect you to pay out a minimum salary of +/- €47.000. Amounts exceeding that number can distributed as dividend.

At this point you have accumulated earnings in the Holding BV through management fees and/or dividend distributions. You can for example choose to reinvest it into the Operating BV, if that company needs extra cash. However, you will most likely want to send most of the profits in the Holding BV to the foreign mother entity. In our case this is a Norwegian AS owning all shares in the Dutch Holding BV.

Because of tax treaties and EU directive, you are able to send profits from the Dutch Holding BV tax free to the Norwegian AS in the form of dividend. One of the main advantages of this setup is that all profits are taxed with Dutch corporate tax. If you send management invoices from the Norwegian AS to one of the Dutch BV's, you will pay the substantially higher Norwegian corporate tax.

Get custom advice

Every situation is unique, but many cases have similar features. If you have any questions about the above, please do not hesitate to contact us using the contact form below.

Exit Strategy: How to Dissolve a BV

"Starting a company is exciting, but knowing how to close one is just as important. In the Netherlands, if your BV has no assets left, we can often perform a Turbo Liquidation, which bypasses months of waiting."

— Thomas, NordicHQ Legal Advisor

Standard Liquidation

- Requires a shareholders' resolution and a formal liquidation period.

- Assets are sold or distributed to shareholders.

- Debts must be settled with all creditors before final de-registration.

Turbo Liquidation (Fast Track)

- Applicable only if the BV has no assets at the time of dissolution.

- The legal entity ceases to exist immediately upon filing.

- Warning: If debts are discovered later, shareholders may be held personally liable.

Mandatory Record Keeping: Even after your BV is gone, Dutch law requires you to keep your administration (records and books) for at least 7 years.

After the company incorporation

There are certain steps you will need to once the company has been registered:

Setting up a bank account. One day after the company is incorporated you will receive your KvK number. You can use that to open a business bank account for you new company.

Deposit the (nominal) share capital in your bank account. Once you have opened your bank account you should deposit the share capital (number of shares x share value) in your bank account with a clear description. Any additional funds can be transferred to the bank account as share premium.

Setting up salary/administration. Your new company will need to setup an administration to pay the salary of the employee(s) as soon as possible. Our accounting partner can assist you in setting up an administration.

Arrange your VAT number. You will receive communication from the Belastingdienst regarding your VAT/BTW number, usually within 5 working days after the registration of your company. With foreign companies we see that this can take up to two weeks. In some cases, the tax authorities sends a letter with additional questions to the company address.

Make sure you are legally compliant by setting up the a few recommended and required legal documents such as GDPR/Privacy agreements and General Terms & Conditions. Create these documents here.

Arrange additional services such as company insurance and a Dutch phone number.

FAQ after the company setup

Transfer of shares in a Dutch BV

In practice, a 'share split' involves a delivery of shares from one shareholder to another, also called a share transfer. In the Netherlands this takes place via a notarial deed. The notary needs the following documents:

- the original shareholders register of the company (the original can be brought to the appointment);

- the number of shares that will be sold and the purchase price thereof;

- a balance sheet of the company, not older than 3 months;

- explanation from a chartered accountant regarding the value of the shares (you should contact your accountant over this);

- Finally, whether there is a change of management and / or a change of address.

A change of shareholder structure can lead to a changing majority in a company. For example when one of two equal partners (both own 50 percent of the shares), sells a part of his or her shares to the other partner.

Change of shareholder structure

One shareholder will in effect become the majority shareholder with the largest share in the company. The other partner will at that point still own a certain percentage of the company, which of course means he has something to say. Legally speaking he still has voting rights/power.

Most shareholders will have a shareholders' agreement in place to determine what will happen in this situation. For example, some clauses in the agreement might require an unanimous decision or a large (2/3) majority. In that case the majority shareholder will still need the partner on board for those decisions. This does not have to intervene with your daily operations, but you should be aware of the consequences.

Shareholders are a major-shareholder/director (or in Dutch: DGA) if they own more than 5% of the company and work for the company. You can together decide to make a new shareholders' agreement / rewrite the old one (same effect) to match the new situation. Furthermore, it important to know if the every director has single representation authority (i.e. any director can make legal decisions for the entire board) or if you have chosen joint representation authority.

Dissolving the BV company

There are a few steps you need to take in order to dissolve a BV company. The first step is to call a meeting of all the shareholders and inform them of your decision to dissolve the company. In order to dissolve the company, you will need to get a majority vote from the shareholders in favour of dissolution. Once the shareholders have voted in favour of dissolution, you will need to file a formal request with the Dutch Chamber of Commerce (Kamer van Koophandel). The Kamer van Koophandel will review your request and if all requirements are met, they will approve the dissolution and issue a certificate of dissolution.

Why would you dissolve a BV?

There are a few reasons why you might decide to dissolve a BV company. One reason might be that the company is no longer profitable and it is not worth continuing to operate. Another reason might be that the company is experiencing financial difficulties and is unable to pay its debts. Dissolving the company can be a way to liquidate its assets and pay off its debts. Finally, it might also be necessary to dissolve a BV company in order to comply with Dutch law. For example, if the company is inactive for a certain period of time or if it fails to file annual reports, it may be required to dissolve the company.

Checklist to ending your BV company

1. Agree with all shareholders

First of all, the Whether the shareholders (if more than 1) have made agreements in person, in the company's deed or in a written shareholders' agreement, the most important thing is that there is agreement among the shareholders to dissolve the BV and end the business.

2. Complete the financials

In this stage you will need to 'clean up' the company to make it empty. In order to do that right, follow the following steps.

Get rid of the company's assets

In order to dissolve your BV, it can no longer have any assets (income) such as stocks and business assets in its books. Check therefore what assets the company still has. The most common assets are:

- debtors

- capital in the bank account

- IP rights

- stocks

- cars and machines

If there is any money left in the bank account after the dissolution and liquidation of the private limited company, it will in principle go to the shareholders. Unless there is a different agreement in the articles of association.

Furthermore, pay off all your loans and end leases. Most importantly, come to an agreement with your creditors.

Cancel also all other agreements and obligations the company has entered into. A few examples are:

- business insurance

- business licences

- telephone numbers and voip

- domain names

- business bank accounts and credit cards.

- subscriptions

- contracts with third parties, employees etc. If you are forced to fire employees, there are special rules you need to follow.

3. Dissolve the BV

To quit your bv, you must have it dissolved. Report the dissolution of your bv to the chamber of commerce via the form 'Dissolution, company, legal entity or partnership'. This is also known as liquidation. The General Meeting of Shareholders takes a formal decision on this. The bv stops when you and any shareholders agree on this decision. You can also choose a future time to wind up the bv.

Turbo liquidation

Turboliquidation is a quick way to dissolve your BV if there are no assets left. You then no longer have any assets in the BV (income). All you need is a dissolution resolution from the General Meeting of Shareholders. Through this resolution, the legal entity (the bv) immediately ceases to exist.

Turbo liquidation is not without risk. A creditor can demand payment through the courts (liquidation) if it turns out afterwards that there are still debts. As a result, shareholders are now personally liable because the legal entity has been dissolved.

4. De-register the BV from the chamber of commerce

After dissolving the BV, the company needs to de-registered from the chamber of commerce (KvK) registrar. This is done by filling in a form.

5. Settle for corporation tax and VAT.

At this stage, the company will receive communication from the tax authorities to perform a final VAT and corporate income tax return.

After following these steps, your company is dissolved, de-registered and settled for taxes. The only thing you will have to do now is keeping your administration for at least 7 years!